FATF’s latest review also reveals that 75% of jurisdictions globally fall short of crypto compliance.

The Financial Action Task Force (FATF) has released its fifth targeted review on the implementation of crypto regulations globally, revealing that while progress has been made, overall compliance remains behind traditional financial sectors.

Stay up-to-date with the latest blockchain developments in Africa

Quick facts

- 75% of assessed jurisdictions are still partially or non-compliant with Recommendation 15 (R 15) on virtual assets.

- Nearly one-third of surveyed jurisdictions have not passed Travel Rule legislation.

- Terrorist groups, particularly in Syria and Asia, are increasingly using virtual assets, often favoring stablecoins.

Be smart: The FATF’s Recommendation 15 requires countries to regulate crypto firms for anti-money laundering and counter-terrorist financing (AML/CFT) purposes. The Travel Rule mandates that crypto companies collect and share customer information for transactions over a certain threshold.

What they’re saying

“A continued lack of implementation of the relevant FATF Standards globally means that VAs and VASPs remain vulnerable to misuse and overall implementation of the Standards remains behind that of other financial sectors.”

Zoom in

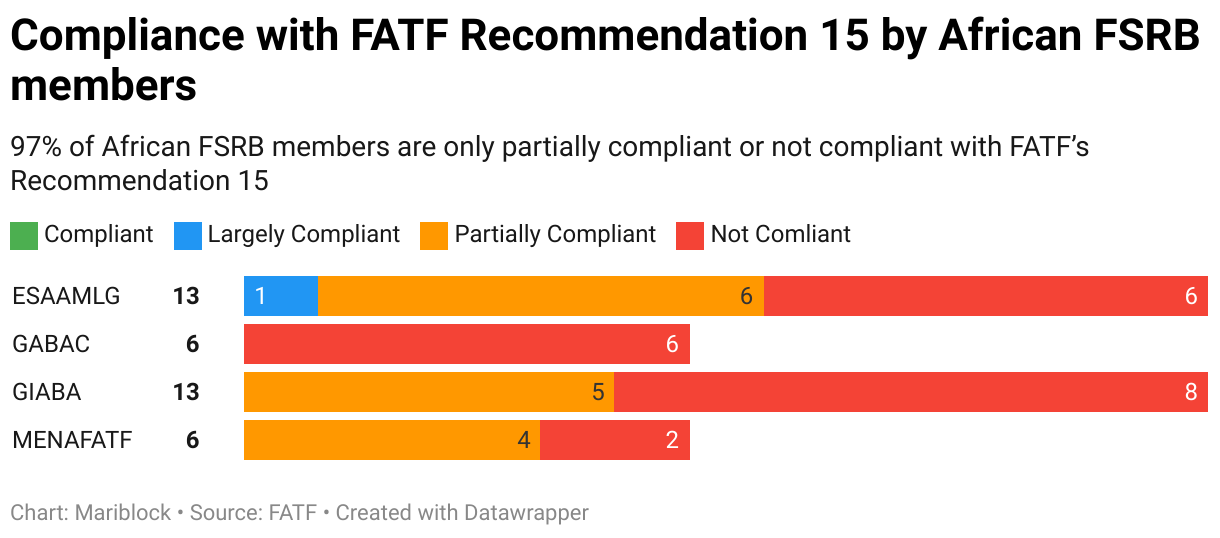

The report also provides insights into the implementation of R 15 across different FATF-Style Regional Bodies (FSRBs).

Be smart: FSRBs are independent bodies partnering with FATF to combat money laundering and terrorist financing worldwide. FATF establishes global standards, while FSRBs adapt and implement these standards regionally. This partnership ensures AML/CFT efforts are both global in scope and tailored to regional needs and contexts.

For Africa, the report shows that approximately 97% of surveyed countries are either only partially compliant or non-compliant with recommendation 15.

Why it matters

Effective regulation is crucial to mitigate money laundering and terrorist financing risks associated with cryptocurrencies.

Zoom out

As crypto adoption continues to grow in Africa, regulators face increasing pressure to implement effective oversight.

- At present, South Africa is the only African economy with materially important crypto activity to have a relatively advanced digital asset regulatory regime.

- The country initially declared crypto as a financial product in 2022.

- As of June 30, 2024, South Africa has granted crypto 138 licenses.

- While Nigeria published a crypto rulebook in 2022, it still doesn’t have a clear licensing regime in place. More recently, it’s taken the regulation-by-enforcement approach, with the country currently in a legal battle with crypto exchange Binance.

Credit: Source link