Citadel Securities’ latest SEC filing and Blockchain Association’s response expose something more consequential: an early public battle over the real prize in tokenized stocks. Wall Street’s goal is to remain indispensable when equities become tokenized.

The establishment’s position on tokenization has moved faster than most observers expected. Citadel Securities says it welcomes tokenization because it can improve outcomes for investors and issuers, including efficiency in clearing and settlement and shareholder engagement.

Nasdaq unveiled an equity token design in March, explicitly designed to preserve regulated market infrastructure, keep public companies at the center of ownership records, and integrate blockchain into the official share registry.

SIFMA told Congress that tokenized securities can enhance market infrastructure, investor access, and capital formation.

Even the SEC is treating tokenized stocks as a live policy category: Commissioner Hester Peirce said in March that staff is working on a narrower innovation exemption for limited trading of certain tokenized securities.

Additionally, Chairman Paul Atkins said market participants should be able to engage with decentralized applications on public, permissionless blockchains if they want to.

That convergence makes the real dispute harder to caricature as old finance versus crypto, as traditional firms favor tokenization. The debate is over whether blockchain is deployed within existing control structures or in ways that reduce them.

The legal fight behind the policy argument

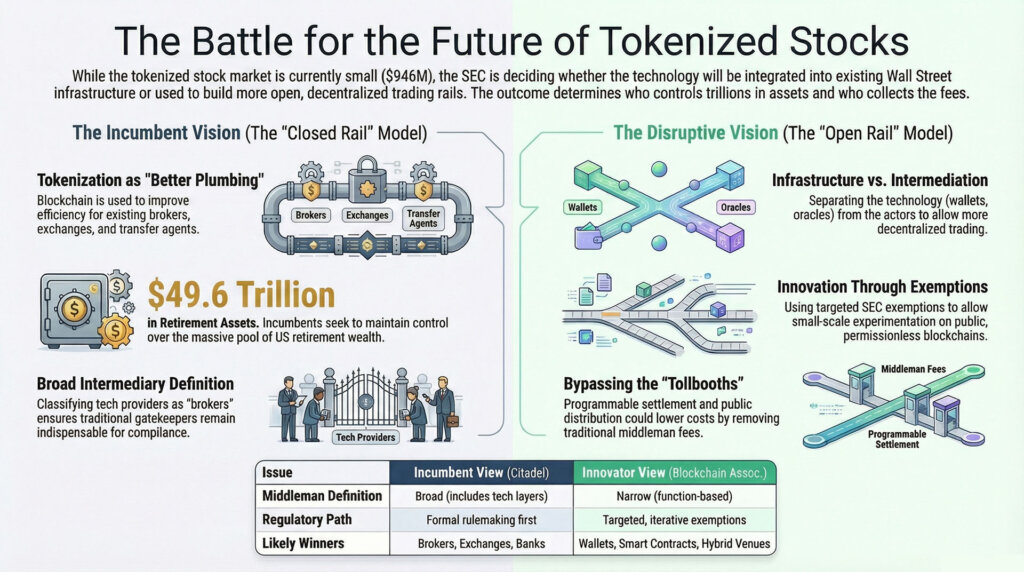

Citadel Securities’ core position is that the SEC should identify the intermediaries involved in tokenized equity trading, avoid broad exemptive relief from the exchange and broker-dealer definitions, and proceed through notice-and-comment rulemaking rather than targeted exemptions.

Its supporting argument, sharpened by economist James Overdahl’s analysis, is that broad relief risks building a parallel regulatory regime with weaker investor protections and more fragmented liquidity.

Blockchain Association’s (BA) response says securities laws regulate actors performing covered market functions, such as brokers, dealers, and exchanges, and that Citadel Securities’ framing would stretch those categories to include validators, front ends, wallets, liquidity providers, oracle providers, and developers in ways that conflate infrastructure with intermediation.

BA also argues the SEC has a long history of using no-action relief and targeted exemptions before formalizing rules, and that forcing tokenized equities through a full rulemaking cycle while the market is still small effectively benefits incumbents by keeping experimentation inside existing pipes.

Intermediaries are where the economics of routing, custody, market-making, settlement, and compliance converge. The regulatory definition of who counts as a middleman determines who gets paid and who gets squeezed.

| Issue | Citadel Securities / incumbent view | Blockchain Association view | What it means in practice |

|---|---|---|---|

| Who counts as intermediary | Broad reading | Narrower, function-based reading | Determines who must register |

| Regulatory path | Rulemaking first | Targeted exemptions / iterative relief | Determines speed of rollout |

| Market structure outcome | Tokenization inside existing rails | Room for more open rails | Decides whether middlemen keep control |

| Likely winners | Brokers, exchanges, transfer agents | Wallets, interfaces, hybrid venues | Decides who captures fees |

| Main stated concern | Investor protection / fragmentation | Category overreach / innovation delay | Competing theories of market safety |

If the SEC adopts Citadel Securities’ broader intermediary logic, tokenized stocks land as better plumbing wrapped around familiar gatekeepers: the broker-dealer stack, exchange infrastructure, and transfer agents all keep their place.

If the SEC leans toward BA’s infrastructure-versus-intermediation distinction, some of that value becomes available to wallets, smart contract venues, and public-chain distribution.

The current tokenized stock market provides a concrete backdrop for that policy choice.

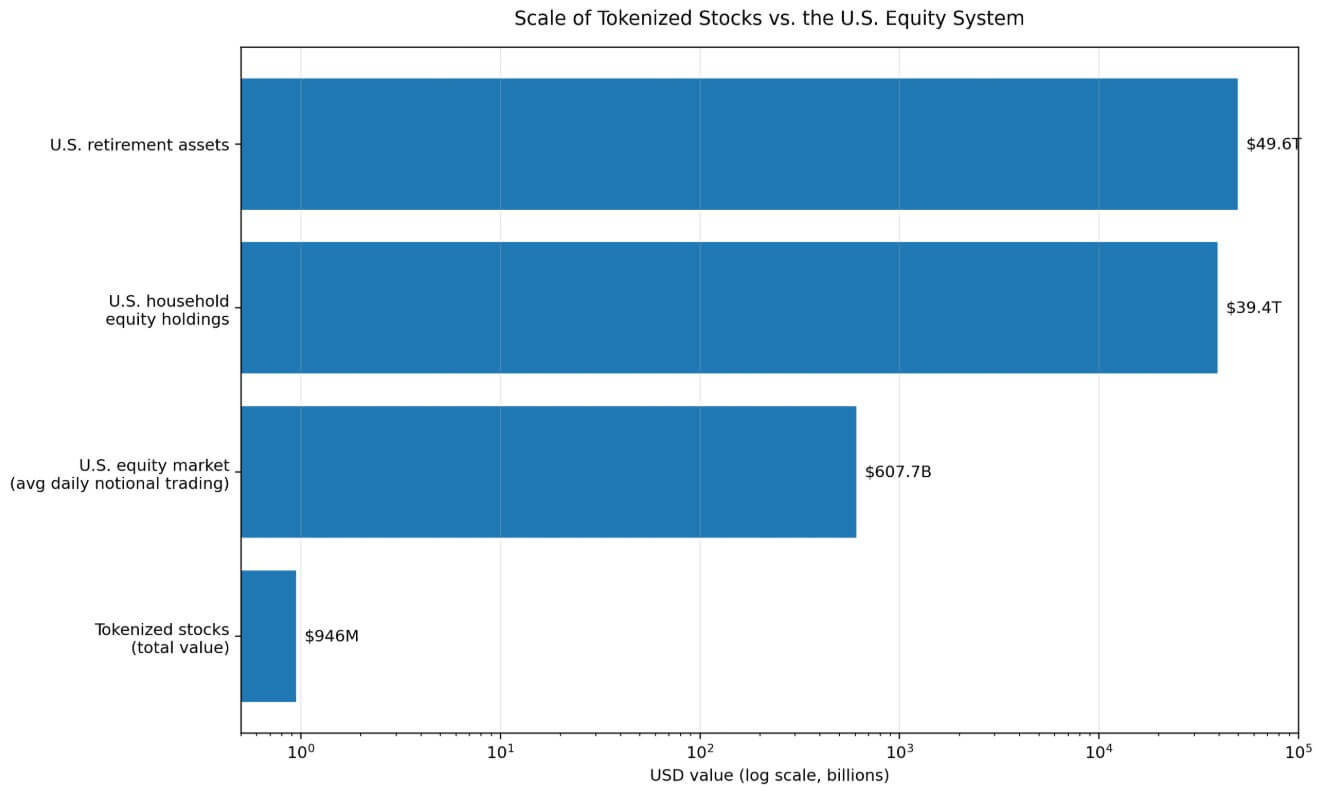

RWA.xyz lists tokenized stocks with a total value of $946 million and a monthly transfer volume of $2.86 billion as of March, across 203,630 holders.

That total sits well below the US equity market, which SIFMA’s 2025 Fact Book shows averaged $607.7 billion in daily notional trading in 2024, against US household equity holdings of roughly $39.4 trillion and total retirement assets of $49.6 trillion.

Policymakers are designing the architecture of a tiny market today.

McKinsey’s 2024 tokenization outlook argues that publicly traded equities are a later-wave asset class precisely because of regulatory complexity, meaning the rules written now will determine who captures that wave once it arrives.

The bullish case

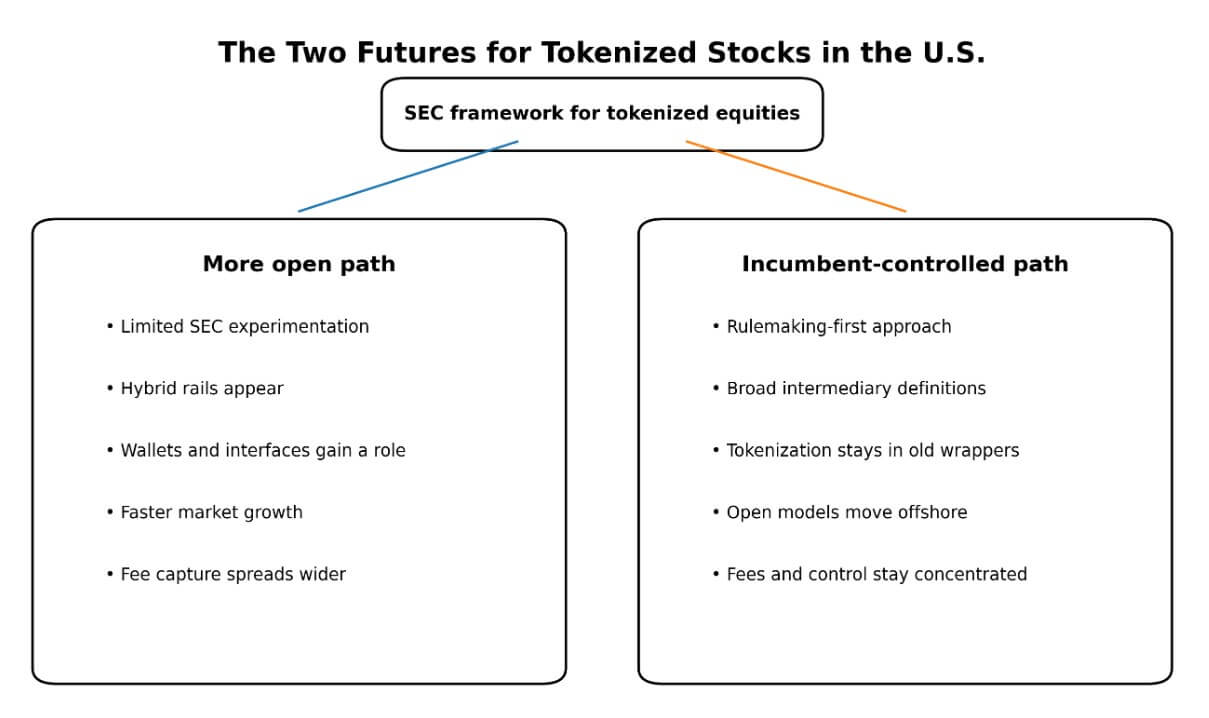

If the SEC allows limited experimentation with novel platforms while still requiring meaningful investor protections, at least some value migrates away from the incumbent stack.

Broker-dealers retain a central role while wallets, interfaces, and smart contract venues perform work that today falls exclusively within the scope of licensed intermediaries. Longer trading hours, programmable settlement, and public chain distribution lower the friction cost of equity ownership in ways that the existing broker architecture cannot easily replicate.

Atkins’s explicit reference to public, permissionless blockchains as a legitimate destination for market participants gives that outcome regulatory backing.

BA’s argument that the SEC can build a targeted, conditional framework through existing exemptive authority also makes the timeline more plausible.

If the exemption moves faster than a full rule, new entrants and new architectures get a window to operate before incumbents can fully shape the final framework through comment cycles.

The $946 million tokenized stock market already demonstrates real transfer activity, indicating that programmability increases turnover even at a small scale.

As overall tokenized RWA markets pass $26 billion and draw institutional attention, tokenized equities in a more open regulatory environment offer clear upside in both outstanding value and fee economics, bypassing the old tollbooths.

Nasdaq’s design, despite its incumbent-friendly framing, also indicates that major exchange operators view tokenization as a growth opportunity rather than a threat.

An SEC framework that preserves investor protections while opening the door to hybrid rails gives even traditional players an incentive to build toward public-chain bridges rather than purely closed systems.

That competition could accelerate technological and user experience improvements, bringing retail equity holders onto on-chain rails faster than current forecasts anticipate.

The bearish case

If the SEC prioritizes formal rulemaking and adopts Citadel Securities’ broader reading of the intermediary definitions, tokenized equities largely stay within the broker-dealer and exchange wrappers.

The user relationship, access control, compliance layer, and settlement legitimacy stay concentrated in familiar hands.

Tokenization becomes better plumbing for the same structure, with faster settlement, cleaner shareholder records, and more efficient corporate actions. The economic distribution of equity market intermediation stays intact.

The IAC draft adds institutional weight to that outcome.

The SEC Investor Advisory Committee’s market-structure recommendation says the Commission should preserve mandatory disclosures, regulation, and oversight of intermediaries, and best-execution-style protections, and explicitly opposes a blanket innovation exemption.

If the final framework reflects IAC-style caution, the most structurally disruptive versions of tokenized equities, those running on public, permissionless chains with non-custodial interfaces, stay outside US regulatory reach.

That regulatory caution carries a second-order consequence that extends beyond domestic markets.

If ambiguity around intermediary definitions keeps the US stuck near the current $946 million tokenized stock base while cleaner frameworks develop offshore, the standard-setting power over the next generation of equity rails migrates with the experimentation.

Incumbents preserve their current position in the short run, but the US financial sector loses the design advantage that comes from being the venue where the architecture proves itself at scale.

SIFMA’s argument that tokenized securities should integrate into the existing federal framework can also read as a slow-roll strategy: integration on incumbent terms, at a rulemaking pace, with established players steering every new architecture through comment cycles they know how to navigate.

Nasdaq’s equity token design illustrates the ceiling of this scenario.

A design explicitly built to preserve issuer control, existing regulatory frameworks, and established market safeguards is technologically interesting and operationally cleaner than today’s infrastructure, with fee and control economics staying concentrated where they are.

If that design becomes the dominant US template, then the more open architectures that could actually reassign intermediary economics stay either offshore or theoretical.

The decision point

The hard part of the tokenization discussion is deciding whether it changes who controls the market.

If the SEC answers that tokenized stocks can exist only inside old channels with old gatekeepers, then tokenization becomes better plumbing for the same structure.

If it leaves room for more open rails, the biggest disruption will be to the firms that used to sit in the middle.

The SEC’s active work now centers on whether the first live US framework preserves the old control stack or leaves room to reassign part of it. That decision will determine who captures the equity token market once it moves from $946 million to the scale that makes the architecture permanent.

Credit: Source link