Crypto exposure may be moving closer to mainstream UK fund portfolios, but the FCA wants it kept at arm’s length.

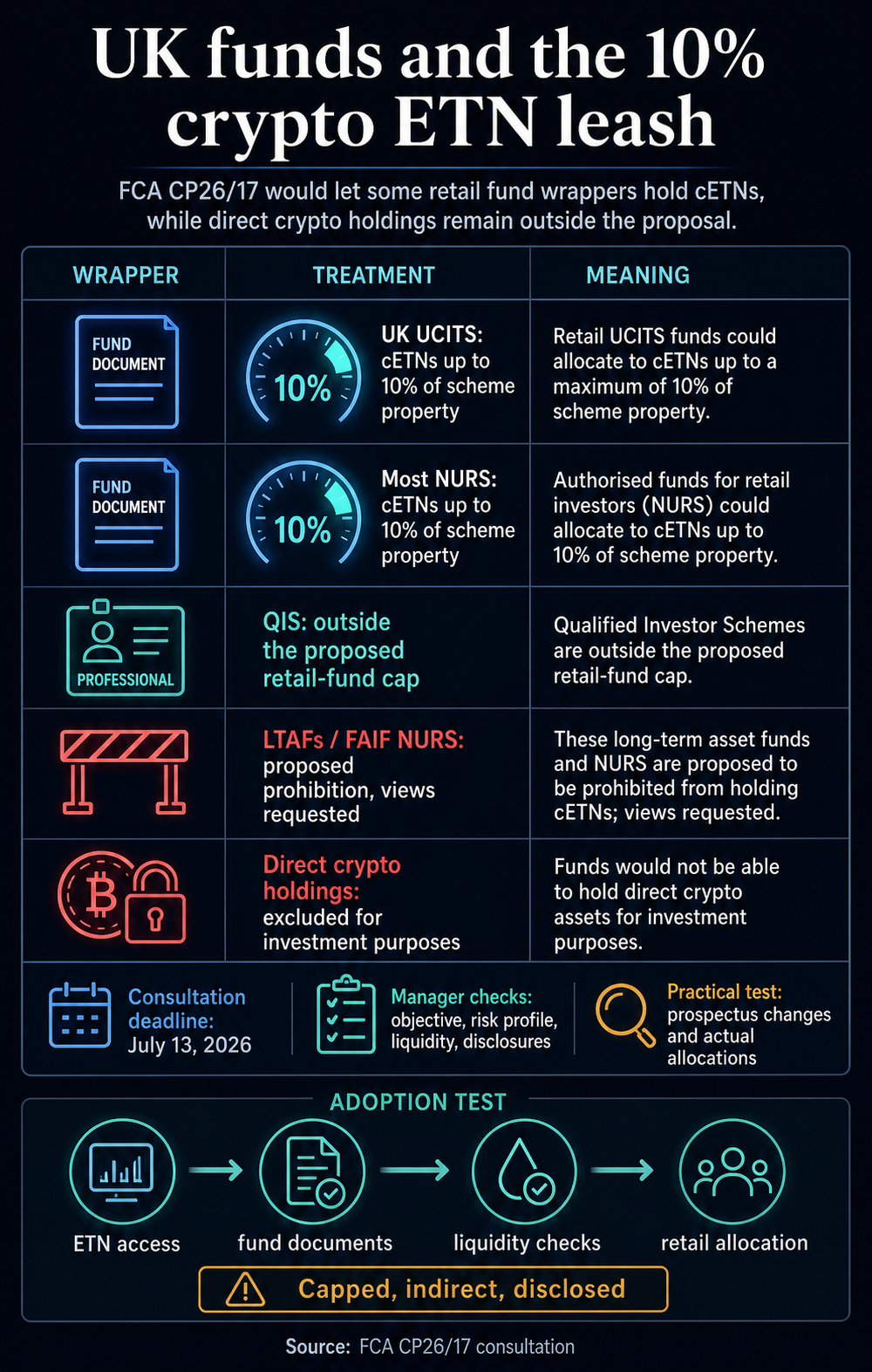

A new proposal would let UCITS schemes and most non-UCITS retail schemes hold crypto exchange-traded notes, capped at 10% of scheme property.

The proposal, set out in the FCA’s CP26/17 consultation, would move crypto exposure deeper into regulated fund plumbing. Retail investors already gained a route to crypto ETNs as standalone exchange products.

The new question is how far those notes can travel inside diversified portfolios run by authorized fund managers.

The answer is a short leash. The FCA would allow a limited ETN sleeve where it matches the fund’s disclosed objective and risk profile.

Direct holdings of Bitcoin, Ether, or other cryptoassets for investment purposes remain outside the proposal. Comments on the fund chapter are due July 13, 2026.

What the cap would allow

The proposed rule would give UK UCITS schemes and, with exceptions, non-UCITS retail schemes a capped allocation channel. The limit would apply at the scheme-property level, meaning up to 10% of a fund’s property could consist of transferable securities that are cryptoasset ETNs.

That threshold makes the exposure possible while keeping it secondary. A balanced multi-asset fund could use the permission as a satellite allocation.

A fund marketed as a conventional retail portfolio would still sit within the retail authorized-fund framework, with crypto exposure contained through the ETN wrapper and the percentage cap.

The FCA also draws lines between fund types. Qualified investor schemes, which are sold to professional clients and sophisticated investors, sit outside the same proposed retail-fund limit.

Long-term asset funds and NURS operating as funds of alternative investment funds face a proposed prohibition on crypto ETN holdings, with the FCA asking for views on that treatment.

| Vehicle | Proposed treatment | Implication |

|---|---|---|

| UK UCITS schemes | May hold cETNs up to 10% of scheme property | Opens a capped route inside mainstream retail fund portfolios |

| Most NURS | May hold cETNs up to 10% of scheme property | Extends the same limited channel beyond UCITS structures |

| Qualified investor schemes | Outside the proposed retail-fund cap | Reflects their professional and sophisticated investor base |

| LTAFs and NURS operating as FAIFs | Proposed prohibition on cETN holdings | Signals that some fund wrappers may remain outside the channel |

| Direct crypto holdings | Excluded for investment purposes | Keeps the exposure indirect through listed notes |

That distinction gives the proposal its shape: access can expand through securities law and fund rules while custody of the coins stays outside the fund portfolio.

A fund could get price-linked crypto exposure through a security traded on a regulated venue. The underlying cryptoasset would remain beyond the authorized fund’s investment holdings.

The proposal follows the FCA’s earlier decision to open retail access to crypto ETNs traded on UK recognized investment exchanges.

That change, which came into force on Oct. 8, 2025, allowed retail consumers to access cETNs through FCA-approved UK investment exchanges, with financial promotion rules and Consumer Duty protections applying.

Those protections kept cETNs in a high-risk category. The FCA said retail cETNs sit outside Financial Services Compensation Scheme coverage, and the ban on retail cryptoasset derivatives remains in place.

The regulator’s stance is that the market has evolved enough to permit controlled access while preserving a high-risk label for the underlying exposure.

That same logic runs through the fund proposal. Crypto ETNs have already become a live UK exchange-traded product category, with London Stock Exchange coverage describing the product segment one year after launch.

For funds, however, the wrapper creates a second layer of responsibility. Managers must decide whether a listed note is eligible and whether the exposure fits a fund’s objectives, liquidity profile, risk limits, and retail disclosures.

That is the trade-off at the center of the proposal. The FCA is opening a controlled route for crypto-linked securities while making fund managers responsible for proving the exposure still fits a retail portfolio.

The FCA says fund managers should have adequate knowledge and understanding of the assets in which a fund invests, conduct due diligence on investment selection, and monitor compliance with the fund’s objective, strategy, risk limits, and liquidity profile.

It also says managers should consider whether cryptoassets and cETNs will remain liquid in stressed conditions.

The cap is the visible control. Disclosure and liquidity work may decide how usable the permission becomes.

The FCA plans to rely on existing disclosure rules for authorized funds holding cETNs. It points managers back to rules on fund objectives, investment policies, marketing communications, Consumer Duty, and risk summaries for cryptoassets and cETNs.

It also says UCITS managers must include a prominent volatility statement where a fund has, or is likely to have, higher volatility in its net asset value.

A manager using the permission would need to explain the exposure in fund documents and consumer-facing materials while keeping the product’s character clear.

A small allocation may still be an essential feature of a strategy when it is more than genuinely de minimis, because crypto ETNs carry different risks from many conventional transferable securities.

The FCA also asks managers to assess cETN holdings against the broader portfolio, including other higher-risk assets, indirect crypto exposure through other funds, and assets correlated with crypto, such as cryptoasset treasury issuers.

A 10% cETN limit therefore leaves a separate question around the rest of a fund’s crypto-linked market behavior.

For retail investors, the practical effect is that crypto can move closer to the default portfolio stack while staying visible. If adopted, the rule would allow a fund to include cETNs, with the exposure disclosed, monitored, and evaluated alongside the rest of the portfolio.

The real adoption test

The proposal creates access; demand still depends on fund managers, platforms, depositaries, and distributors deciding that the capped exposure is worth the documentation, governance, and suitability work.

One path is meaningful, limited adoption. Managers could use cETNs as a small allocation tool inside diversified funds.

In that case, the FCA’s rule would mark a real shift: crypto exposure would move beyond a standalone retail decision or a professional-investor product and become something a mainstream fund could include with risk controls around it.

Another path is largely symbolic. Managers may decide that the 10% limit, disclosure duties, liquidity questions, and reputational risk outweigh the benefit.

The permission would remain a bridge that few products cross, creating a policy change with a modest allocation footprint.

That is why the proposal is best read as an incremental normalization of the crypto market structure rather than a broad portfolio opening.

The FCA is accepting that crypto ETNs have become sufficiently established to be included in some authorized funds, while still trying to prevent their exposure from becoming a dominant risk in retail portfolios.

The next test is practical rather than theoretical. If managers start updating prospectuses, risk summaries, and platform materials after the consultation closes, the 10% cap becomes a real allocation channel. If they hold back, the rule will mark policy permission without much portfolio adoption.

Credit: Source link