The Bank of England has removed the biggest usability objection from its sterling stablecoin plan, but it has kept a ceiling on how large any single systemic pound token can become.

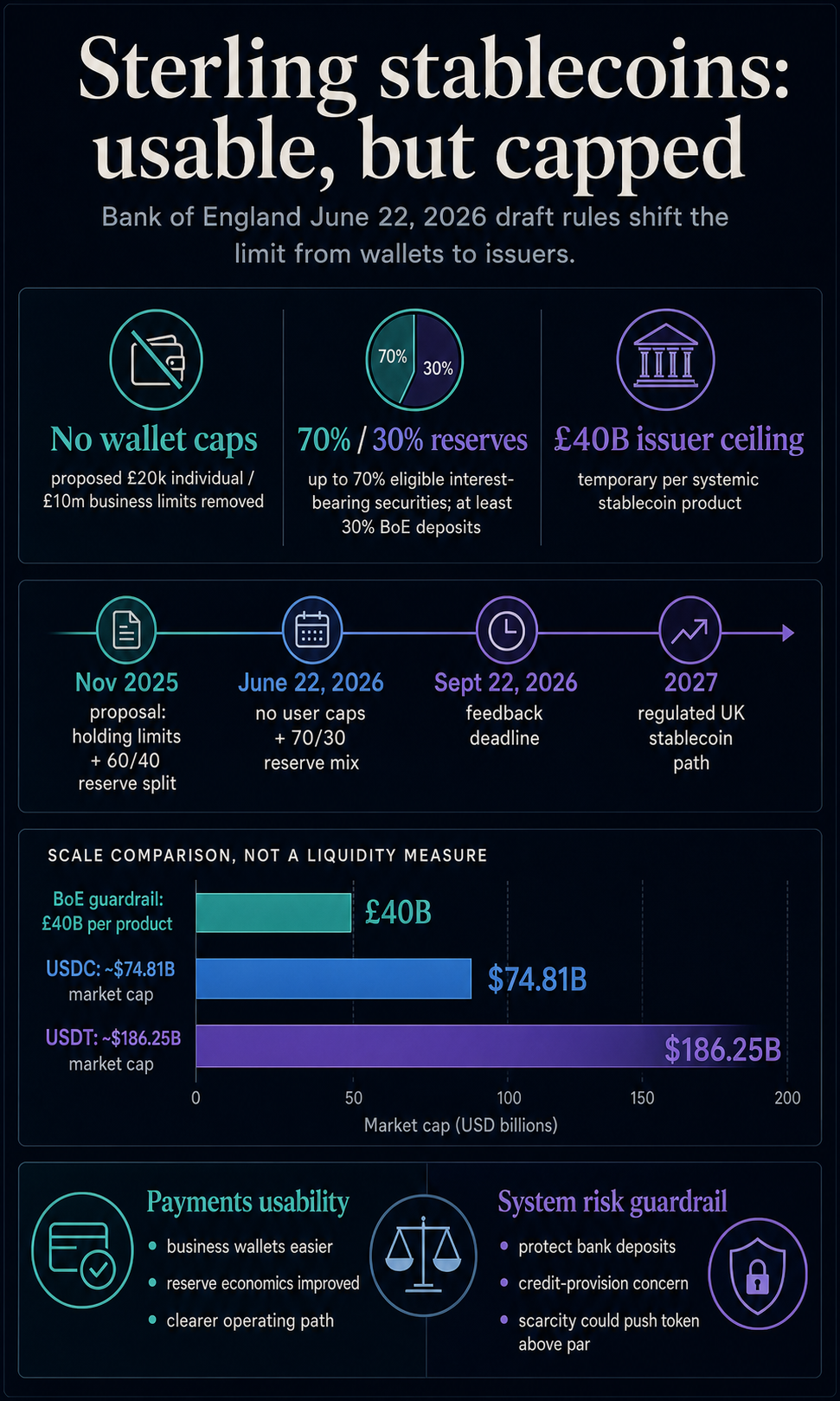

In a June 22 policy statement and draft Code of Practice, the central bank removed proposed holding limits for individuals and businesses, raised the share of backing assets that may be held in interest-bearing securities, and replaced wallet-level caps with a temporary £40 billion issuance guardrail for each systemic sterling stablecoin product.

That turns the UK debate to scaling. A token that no longer has to police ordinary business balances is more plausible as a payments infrastructure, but a successful issuer would still be rationed before it reaches the market cap of the largest dollar tokens.

The result is a different rationing model.

The UK is paving the way for regulated pound tokens to operate from 2027, while reserving the right to slow their growth until the Bank is satisfied that stablecoins will not drain deposits from the banking system quickly enough to undermine access to credit.

From wallet caps to a product ceiling

The Bank’s draft rules consultation closes on Sept. 22, 2026, with the Code of Practice intended to be finalized by the end of the year. Regulated stablecoins are expected to operate in the UK from 2027.

Under the November 2025 proposal, the Bank had considered temporary per-coin holding limits of £20,000 for individuals and £10 million for businesses.

It also proposed a reserve mix that would have allowed up to 60% of backing assets to be in short-term UK government debt and required at least 40% to be in unremunerated Bank deposits.

The new policy statement says those user-level limits will not be implemented. Instead, each systemic stablecoin product will initially be subject to a £40 billion issuance maximum.

The reserve split also moves in issuers’ favor: up to 70% of the backing assets may be held in interest-bearing short-term UK government debt, while the remaining 30% must be held in central bank deposits.

| BoE change | What it improves | What still limits scale |

|---|---|---|

| No proposed individual or business holding caps | More practical wallet and business payment use | Total supply is capped per systemic product |

| 70% backing assets allowed in eligible interest-bearing securities | Better issuer economics than the prior 60% allowance | 30% still sits in unremunerated Bank deposits |

| £40 billion temporary issuance guardrail | Less operational complexity than policing user balances | A successful token can hit a product-level ceiling |

| 2027 operating path | Clearer timing for regulated sterling rails | Dollar tokens have more time to deepen their market lead |

The first point naturally centers on the disappearance of proposed wallet caps and the 2027 path. Those changes make a systemic sterling token more usable than the earlier proposal.

The constraint simply moved.

The June framework answers one question that had hung over the UK regime: whether systemic sterling stablecoins would be too awkward to use in ordinary payment flows.

Removing holding limits gives wallets, merchants, and large businesses a cleaner product surface. Raising the interest-bearing reserve allowance also gives issuers a better chance of building a business without relying only on transaction fees, data advantages, or distribution.

The UK’s work on stablecoins is already practical rather than theoretical. The FCA’s stablecoins sandbox cohort includes firms testing UK stablecoin services, including Monee, ReStabilise, Revolut, and VVTX.

The Bank’s guardrail would apply only if a product is recognized as systemic and enters the Bank’s regime, not to every sandbox test by default.

But those experiments show why the rule design has consequences before full launch: issuers need to know whether a product can serve real payment flows if it succeeds.

The answer is now more constructive than it was under the earlier design. A sterling token can be built around use, not around compliance with individual balance checks.

Once a token becomes large enough to affect payment flows, the question becomes whether the £40 billion ceiling leaves enough room for the exchange support, working balances, and network effects that dollar tokens already enjoy.

CryptoSlate market data shows the gap. USDT has a market capitalization of roughly $186 billion, while USDC has around $74 billion.

A £40 billion cap translates to around $53 billion, well below either of the top dollar coins.

As a scale test, the gap remains clear: a single systemic pound token would start with a ceiling well below USDT and below the combined market cap of the two largest dollar stablecoins.

For crypto markets, the relevant question is practical integration. If a sterling token is capped before it reaches a comparable scale, it can still be useful for UK payments, but it may remain mostly domestic while dollar tokens retain the deeper base of market activity.

Why the pound stablecoin guardrail remains

The Bank’s case is that unrestricted adoption could withdraw money from bank deposits too quickly. Its policy statement describes the guardrail as a transitional measure to mitigate risks to credit provision.

It also says the Bank expects to review, loosen, and ultimately remove the cap once it is satisfied those risks have been addressed.

That point is important because the guardrail is presented as a temporary financial-stability tool rather than a permanent size limit.

The Bank says the £40 billion starting level was calibrated using the same analytical framework that supported the earlier holding-limit proposal.

In its view, the product-level ceiling achieves similar financial-stability protection while avoiding the technical and privacy problems of enforcing limits across wallets, businesses, smart contracts, and intermediaries.

The House of Lords Financial Services Regulation Committee had already pressed the issue. Its June 3 report said the UK risked falling behind the US and EU and urged reconsideration of holding limits, unremunerated backing-asset requirements, and restrictions on commercial banks issuing stablecoins.

CryptoSlate’s earlier coverage noted that the prior caps could have made a pound stablecoin market uneconomic before launch.

The Bank has moved on two of the pressure points, but not all of them. It has abandoned the proposed user limits and eased the reserve split.

It has not removed the non-yielding central-bank-deposit requirement, and the latest statement does not clearly loosen the commercial-bank-issuance question highlighted by lawmakers.

The Bank also acknowledges a new risk created by the issuance-cap model. If demand for a systemic stablecoin exceeds capped supply, the token could trade above par in secondary markets.

That is a different problem from the usual fear of a stablecoin falling below its peg.

In this case, scarcity could make the token too expensive because users want more of it than issuers are allowed to create.

The Bank says that risk is manageable and would likely require a sustained, large-scale flow into a systemic stablecoin.

Still, the admission shows the tradeoff clearly. User caps would have directly hurt adoption.

Issuer caps protect the banking system more cleanly, but they can turn success into a supply problem.

The 2027 test will be adoption before dollar scale hardens

The June framework gives sterling stablecoins a clearer route. The decision for issuers, wallets, and payments firms is whether that route lets them become useful quickly enough.

The broader UK crypto regime is also moving toward 2027, with the FCA outlining the path for firms preparing under the new framework.

That timeline gives issuers and infrastructure providers a year to prepare, while dollar stablecoins have more time to extend their lead in crypto trading and on-chain payment flows.

For the UK, that creates a split outcome. The Bank has made systemic sterling stablecoins more viable as domestic payment infrastructure.

It has also kept enough controls in place to prevent any single-pound token from immediately competing with the largest dollar tokens in terms of size. Both can be true at once.

The next signal is whether the £40 billion guardrail remains comfortably above early adoption or becomes the first hard ceiling a successful issuer must negotiate.

If sterling stablecoins stay mainly inside UK payment and sandbox use cases, the cap may look generous.

If banks, fintechs, exchanges, and tokenized-asset platforms converge around a single product, the ceiling could become the story.

That is the market test the Bank has created. Sterling stablecoins now have a more usable rulebook. Dollar stablecoins still have the scale.

The race turns on whether UK issuers can build enough real payment demand before the temporary guardrail becomes the measure of how far pound tokens are allowed to run.

Credit: Source link