Strategy, the Bitcoin treasury and enterprise software company formerly known as MicroStrategy, has spent years turning public markets into a funding engine for Bitcoin purchases. That model helped make the company the world’s largest corporate holder of the digital asset.

Now, the securities used to power that strategy are flashing stress.

The pressure is centered on STRC, Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock, a key funding instrument designed to trade near a stated amount of $100.

Instead, STRC fell to a record low near $71 on Friday before recovering to about $75, leaving it roughly 25% below par and raising questions about whether the company can continue raising capital on favorable terms.

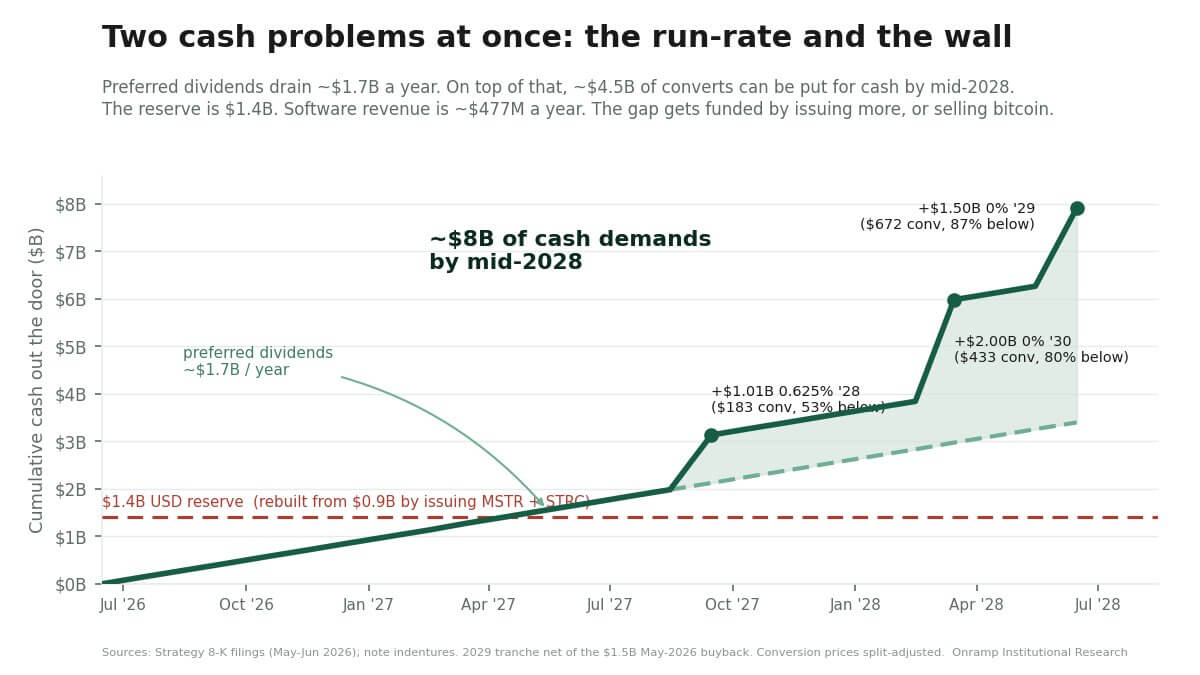

The selloff comes as Strategy faces what some market participants describe as an $8 billion cash wall over the next two years, including preferred dividend obligations and convertible debt that holders may be able to put back to the company for cash before final maturity.

The strain has shifted investor attention away from the size of Strategy’s Bitcoin holdings and toward the balance sheet built around them.

Strategy loses its Bitcoin premium

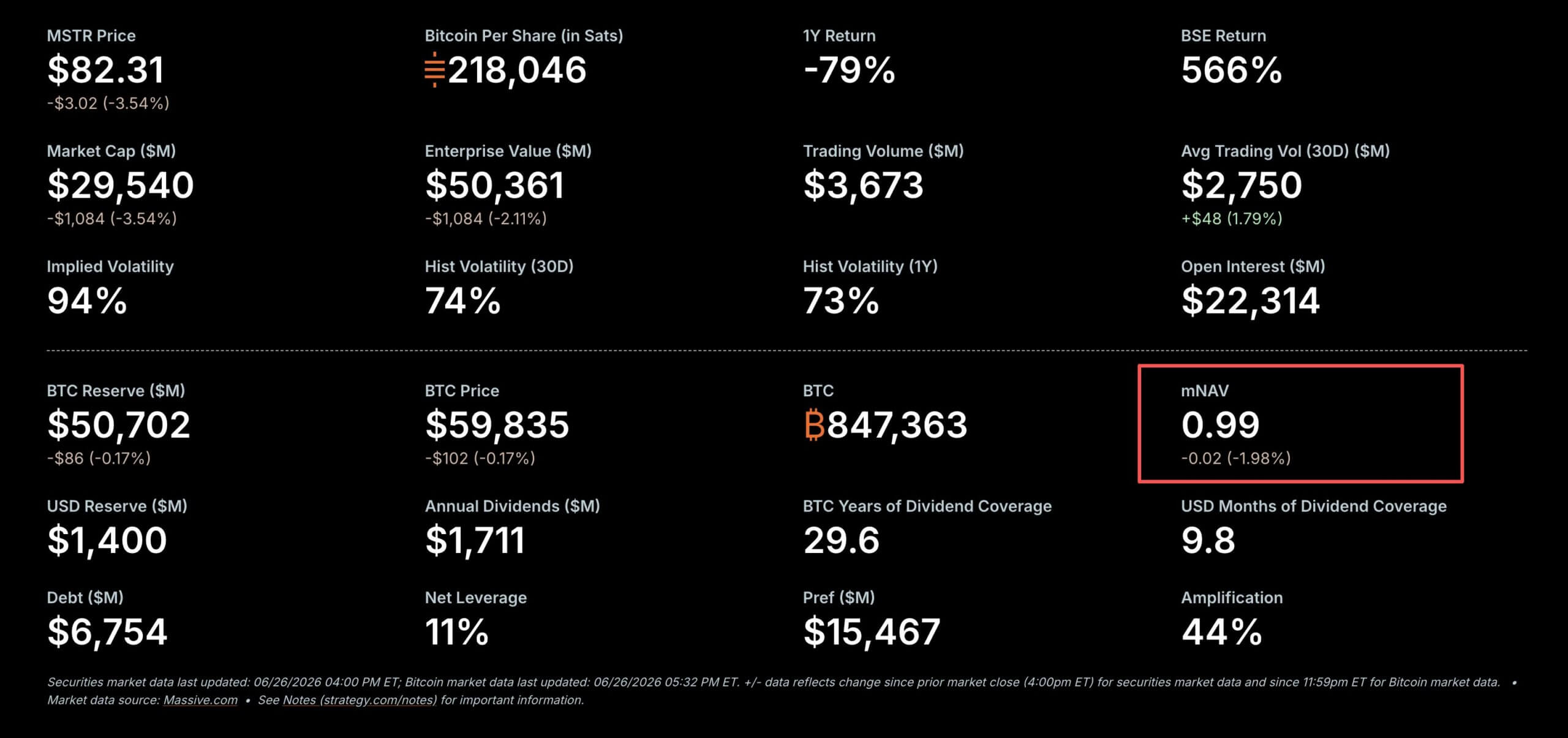

That change became clear Friday when Strategy’s enterprise market-to-net asset value slipped below 1, briefly erasing the premium that had long separated the company from other corporate Bitcoin holders.

The metric is important because it looks beyond the spot value of Strategy’s Bitcoin. It incorporates the company’s debt, cash, and preferred equity, offering a fuller picture of how public markets value the entire structure Saylor has built around the asset.

So, when it is below parity, this suggests investors are no longer paying extra for Strategy’s ability to accumulate Bitcoin through public-market financing. Instead, they are discounting the complexity and cost of the claims sitting around the company’s treasury.

That marks a reversal from the trade that helped define Strategy’s rise. For years, the company could sell stock or other securities at elevated valuations and use the proceeds to buy more Bitcoin.

The premium created a powerful loop where the higher market value helped fund more purchases, and more purchases reinforced the company’s status as the leading listed Bitcoin proxy.

But the same loop becomes harder to sustain when the common stock and preferred shares fall together.

Indeed, Strategy’s common shares fell to a two-year low of $82 on Friday. Bitcoin, meanwhile, was also struggling under the $60,000 mark.

For shareholders, the concern is no longer only the direction of Bitcoin. It is whether Strategy can keep using capital markets on terms that do not deepen dilution, raise cash costs, or put pressure on its holdings.

Strategy faces an $8 billion cash test

Meanwhile, the debate around Strategy is increasingly moving away from Bitcoin alone and toward a simpler question: how much cash the company may need if markets remain hostile.

Glenn Cameron, global head of institutional at Ooramp Bitcoin, estimates that Strategy could face about $8 billion in potential cash demands over the next two years.

According to him, the pressure comes from two places: the preferred-stock stack used to finance Bitcoin purchases and convertible debt that may have to be repaid in cash if the common stock stays depressed.

The preferred shares are already creating a heavy run-rate. Cameron puts Strategy’s annual preferred dividend burden near $1.7 billion, with STRC alone accounting for roughly $1.2 billion. That estimate is based on about 104.9 million STRC shares and an 11.5% annualized rate on the preferred stock’s $100 stated amount.

The strain grows as STRC trades further below par. The preferred was structured with a variable dividend rate intended to help pull the security toward its $100 stated value.

However, a higher rate also raises the cost of keeping the instrument attractive to investors, particularly when the market is demanding a bigger yield to hold junior Strategy exposure.

At about $75, STRC’s effective yield rises to roughly 15%, a sign that investors want far more compensation than the stated dividend rate suggests.

While that does not mean Strategy is facing an immediate liquidity event, it shows that the preferred has moved from a cheap financing tool into a more expensive part of the capital structure.

The second pressure point is convertible debt. Cameron has identified roughly $4.5 billion of notes that holders may be able to put back to Strategy for cash between September 2027 and June 2028.

The potential repayment dates include about $1.01 billion on Sept. 15, 2027, $2 billion on March 1, 2028, and roughly $1.5 billion on June 1, 2028.

Those notes become more important when Strategy’s common stock trades far below the conversion prices. If the shares remain deeply out of the money, holders have less reason to convert into equity and more reason to seek cash repayment where the terms allow it.

That is how the cash wall approaches the $8 billion figure: preferred dividends running in the background, combined with convertible notes that could require cash inside a concentrated window.

Strategy has about $1.4 billion in cash reserves against those potential demands. The company has rebuilt part of that buffer after earlier drawing it down, but it did so by selling securities into a weaker market. That helped preserve liquidity, while also raising the risk of further dilution.

Thus, the company’s choices are becoming more constrained. It can sell more common stock, issue more preferred shares, refinance debt, slow Bitcoin purchases, or sell some of its Bitcoin holdings.

However, none of those options is cost-free.

Common-stock issuance dilutes existing holders. More preferred stock adds to the dividend burden. Refinancing depends on investor appetite at a time when Strategy-linked securities are under pressure.

At the same time, slower Bitcoin purchases would weaken the accumulation story that has defined the company. Selling Bitcoin would be the sharpest break from a strategy built around indefinite accumulation.

STRC trades like ‘junk credit’ as bears target $60

STRC’s decline has drawn comparisons with past crypto failures, but the stress in Strategy’s preferred stock is moving through a different mechanism.

Blockchain intelligence firm Arkham Intelligence has pushed back against comparisons between STRC and Terra’s LUNA, arguing that Strategy’s preferred stock does not operate like an algorithmic stablecoin. There is no automatic peg-defense mechanism, and a drop below the $100 stated amount does not by itself trigger a liquidation event.

That distinction is important because STRC is a perpetual preferred security, not a redeemable token. It sits below Strategy’s debt in the capital stack, has no fixed maturity date, and does not require the company to buy it back at par on a set schedule. Its dividends are cumulative, but cash payments still depend on board approval and the company’s ability to fund them.

Those features give Strategy more flexibility than crypto structures built around forced redemptions or collateral liquidations. They also explain why STRC can trade far below par without producing an immediate mechanical collapse.

The market is sending a different warning. STRC is no longer being valued as a security that will naturally return to its $100 stated amount. Investors are treating it more like a yield-bearing claim on Strategy’s ability to keep paying dividends, preserve cash, and raise capital while Bitcoin remains under pressure.

That has pushed STRC closer to the language of stressed corporate credit than crypto-native leverage. At roughly 25% below par, the preferred stock reflects a higher required return for investors taking exposure to one of the company’s junior obligations.

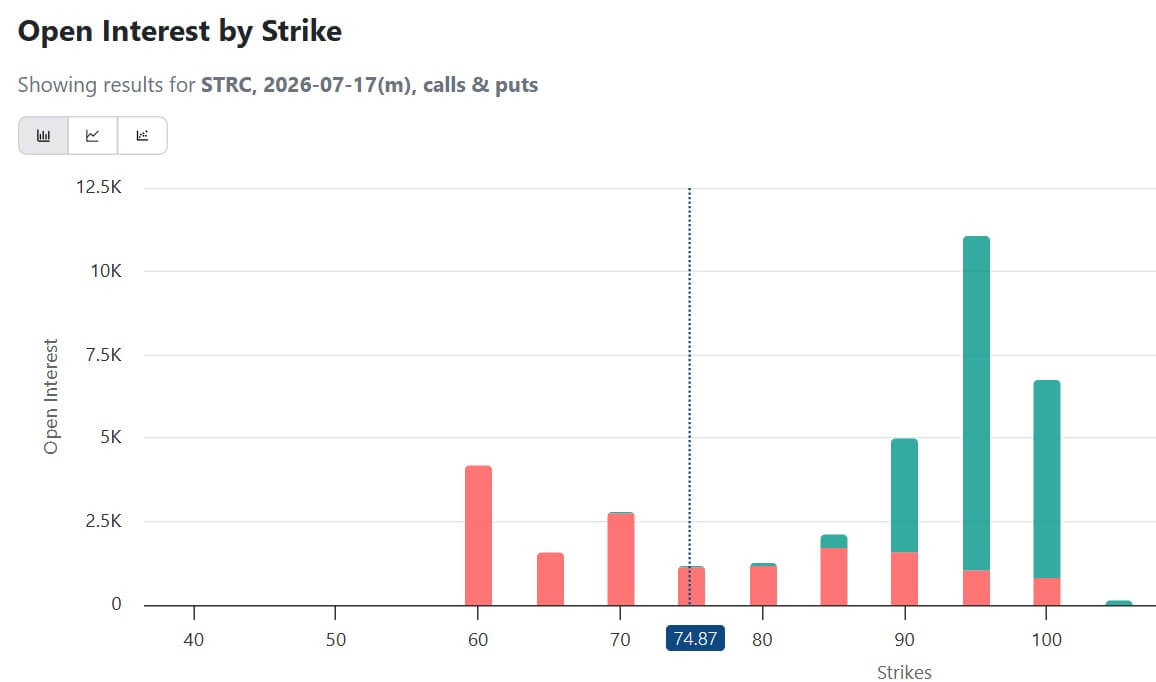

Notably, that pressure is now showing up in the options market. Traders have built bearish positions around STRC, with notable open interest in July 17 contracts at the $60 strike.

The positioning suggests some investors are preparing for a deeper downside if confidence in the preferred stock continues to erode.

Strategy’s Bitcoin model comes under fire

The strain across Strategy’s securities has opened the company to sharper criticism from across the digital asset industry.

Ripple Chief Executive Officer Brad Garlinghouse used a CNBC interview on Friday to discuss Saylor’s financing strategy, arguing that the company’s reliance on preferred equity and other capital-markets tools has pulled attention away from what ultimately gives digital assets value.

According to him:

“Financial engineering does not drive long-term value. The long-term value of any digital asset is going to be driven by utility.”

Garlinghouse said he remains bullish on Bitcoin, but pointed to STRC’s decline as evidence that Strategy’s model is under pressure. He added:

“Team Michael Saylor wasn’t focused on the right stuff and that has hurt the overall market.”

The comments underline a widening philosophical divide in crypto. Saylor’s approach is built around Bitcoin scarcity, public-market access, and repeated accumulation. Garlinghouse’s critique reflects a utility-first view of digital assets, centered more on payments, settlement, and tokenized financial infrastructure.

That disagreement has existed for years. However, what has changed is that the market is now giving critics new evidence.

As long as Bitcoin rose and Strategy’s securities traded at a premium, the company’s model appeared self-reinforcing. It could sell securities, buy more Bitcoin, and use investor enthusiasm to fund the next round of accumulation. Falling STRC, weaker MSTR, and a shrinking enterprise mNAV have made the same structure look more vulnerable.

However, Michael Saylor has rejected these concerns, saying:

“Volatility tests every capital structure. Strategy remains focused on Bitcoin, disciplined capital allocation, credit quality, and long-term value creation.”

The next test would be whether Strategy can repair confidence without weakening the strategy that made it one of the most important Bitcoin proxies in public markets.

Credit: Source link